Page 50 - CityofEulessFY26AdoptedBudgetOrdinance2432

P. 50

2025 Tax Rate Calculation Worksheet - Taxing Units Other Than School Districts or Water Districts Form 50- 856

Amount/ Rate

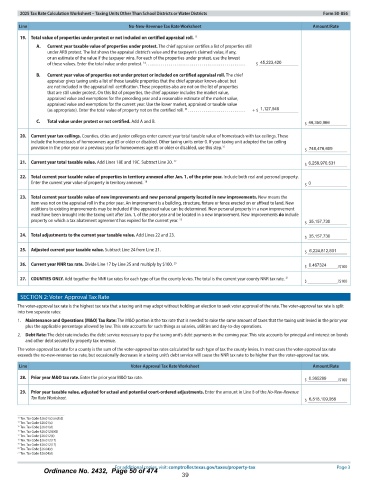

19. Total value of properties under protest or not included on certified appraisal roll. 13

A. Current year taxable value of properties under protest. The chief appraiser certifies a list of properties still

under ARB protest. The list shows the appraisal district' s value and the taxpayer' s claimed value, if any,

or an estimate of the value if the taxpayer wins. For each of the properties under protest, use the lowest

45,223,420

of these values. Enter the total value under protest.'^

B. Current year value of properties not under protest or included on certified appraisal roll. The chief

appraiser gives taxing units a list of those taxable properties that the chief appraiser knows about but

are not included in the appraisal roll certification. These properties also are not on the list of properties

that are still under protest. On this list of properties, the chief appraiser includes the market value,

appraised value and exemptions for the preceding year and a reasonable estimate of the market value,

appraised value and exemptions for the current year. Use the lower market, appraised or taxable value

1, 127, 546

as appropriate). Enter the total value of property not on the certified roll. 15

C. Total value under protest or not certified. Add A and B. 46, 350, 966

20. Current year tax ceilings. Counties, cities and junior colleges enter current year total taxable value of homesteads with tax ceilings. These

include the homesteads of homeowners age 65 or older or disabled. Other taxing units enter 0. If your taxing unit adopted the tax ceiling

provision in the prior year or a previous year for homeowners age 65 or older or disabled, use this step.16 748, 476,609

21. Current year total taxable value. Add Lines 18E and 19C. Subtract Line 20. 17 6, 259, 970, 531

22. Total current year taxable value of properties in territory annexed after Jan. 1, of the prior year. Include both real and personal property.

Enter the current year value of property in territory annexed. 18 0

23. Total current year taxable value of new improvements and new personal property located in new improvements. New means the

item was not on the appraisal roll in the prior year. An improvement is a building, structure, fixture or fence erected on or affixed to land. New

additions to existing improvements may be included if the appraised value can be determined. New personal property in a new improvement

must have been brought into the taxing unit after Jan. 1, of the prior year and be located in a new improvement. New improvements do include

property on which a tax abatement agreement has expired for the current year. 19 35, 157, 730

24. Total adjustments to the current year taxable value. Add Lines 22 and 23. 35, 157,730

25. Adjusted current year taxable value. Subtract Line 24 from Line 21. 6, 224,812,801

26. Current year NNR tax rate. Divide Line 17 by Line 25 and multiply by $ 100. 2° 0. 467324 100

27. COUNTIES ONLY. Add together the NNR tax rates for each type of tax the county levies. The total is the current year county NNR tax rate. 21 100

SECTION 2: Voter Approval Tax Rate

The voter -approval tax rate is the highest tax rate that a taxing unit may adopt without holding an election to seek voter approval of the rate. The voter -approval tax rate is split

into two separate rates:

1. Maintenance and Operations ( M& O) Tax Rate: The M& O portion is the tax rate that is needed to raise the same amount of taxes that the taxing unit levied in the prior year

plus the applicable percentage allowed by law. This rate accounts for such things as salaries, utilities and day-to- day operations.

2. Debt Rate: The debt rate includes the debt service necessary to pay the taxing unit's debt payments in the coming year. This rate accounts for principal and interest on bonds

and other debt secured by property tax revenue.

The voter -approval tax rate for a county is the sum of the voter -approval tax rates calculated for each type of tax the county levies. In most cases the voter -approval tax rate

exceeds the no -new -revenue tax rate, but occasionally decreases in a taxing unit' s debt service will cause the NNR tax rate to be higher than the voter -approval tax rate.

oter-Approval Tax Rate Worksh

28. Prior year M& O tax rate. Enter the prior year M& O tax rate. 0. 365289

100

29. Prior year taxable value, adjusted for actual and potential court -ordered adjustments. Enter the amount in Line 8 of the No -New -Revenue

Tax Rate Worksheet. $ 6, 518, 109, 056

Tex. Tax Code § 26.01( c) and (d)

Tex. Tax Code § 26.01( c)

s Tex. Tax Code § 26.01( d)

19 Tex. Tax Code § 26. 012( 6)( B)

Tex. Tax Code § 26.012( 6)

1e Tex. Tax Code § 26. 012( 17)

Tex. Tax Code § 26.012( 17)

Tex. Tax Code § 26.04( c)

Tex. Tax Code § 26.04( d)

4 visit: comptroller. texas. gov/ taxes/ property- tax Page 3

U

Ordinance No. 2432, gagedgiQnaallio4

39