Page 251 - Grapevine FY22 Adopted Budget v2

P. 251

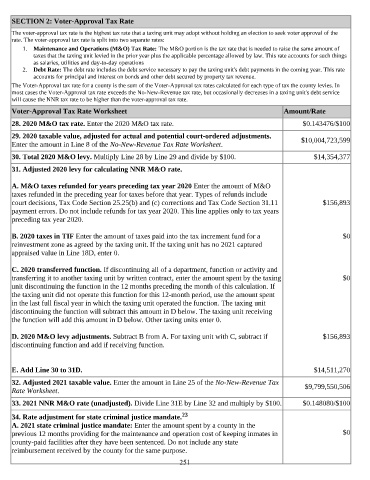

SECTION 2: Voter-Approval Tax Rate

The voter-approval tax rate is the highest tax rate that a taxing unit may adopt without holding an election to seek voter approval of the

rate. The voter-approval tax rate is split into two separate rates:

1. Maintenance and Operations (M&O) Tax Rate: The M&O portion is the tax rate that is needed to raise the same amount of

taxes that the taxing unit levied in the prior year plus the applicable percentage allowed by law. This rate accounts for such things

as salaries, utilities and day-to-day operations

2. Debt Rate: The debt rate includes the debt service necessary to pay the taxing unit's debt payments in the coming year. This rate

accounts for principal and interest on bonds and other debt secured by property tax revenue.

The Voter-Approval tax rate for a county is the sum of the Voter-Approval tax rates calculated for each type of tax the county levies. In

most cases the Voter-Approval tax rate exceeds the No-New-Revenue tax rate, but occasionally decreases in a taxing unit's debt service

will cause the NNR tax rate to be higher than the voter-approval tax rate.

Voter-Approval Tax Rate Worksheet Amount/Rate

28. 2020 M&O tax rate. Enter the 2020 M&O tax rate. $0.143476/$100

29. 2020 taxable value, adjusted for actual and potential court-ordered adjustments. $10,004,723,599

Enter the amount in Line 8 of the No-New-Revenue Tax Rate Worksheet.

30. Total 2020 M&O levy. Multiply Line 28 by Line 29 and divide by $100. $14,354,377

31. Adjusted 2020 levy for calculating NNR M&O rate.

A. M&O taxes refunded for years preceding tax year 2020 Enter the amount of M&O

taxes refunded in the preceding year for taxes before that year. Types of refunds include

court decisions, Tax Code Section 25.25(b) and (c) corrections and Tax Code Section 31.11 $156,893

payment errors. Do not include refunds for tax year 2020. This line applies only to tax years

preceding tax year 2020.

B. 2020 taxes in TIF Enter the amount of taxes paid into the tax increment fund for a $0

reinvestment zone as agreed by the taxing unit. If the taxing unit has no 2021 captured

appraised value in Line 18D, enter 0.

C. 2020 transferred function. If discontinuing all of a department, function or activity and

transferring it to another taxing unit by written contract, enter the amount spent by the taxing $0

unit discontinuing the function in the 12 months preceding the month of this calculation. If

the taxing unit did not operate this function for this 12-month period, use the amount spent

in the last full fiscal year in which the taxing unit operated the function. The taxing unit

discontinuing the function will subtract this amount in D below. The taxing unit receiving

the function will add this amount in D below. Other taxing units enter 0.

D. 2020 M&O levy adjustments. Subtract B from A. For taxing unit with C, subtract if $156,893

discontinuing function and add if receiving function.

E. Add Line 30 to 31D. $14,511,270

32. Adjusted 2021 taxable value. Enter the amount in Line 25 of the No-New-Revenue Tax $9,799,550,506

Rate Worksheet.

33. 2021 NNR M&O rate (unadjusted). Divide Line 31E by Line 32 and multiply by $100. $0.148080/$100

34. Rate adjustment for state criminal justice mandate. 23

A. 2021 state criminal justice mandate: Enter the amount spent by a county in the

previous 12 months providing for the maintenance and operation cost of keeping inmates in $0

county-paid facilities after they have been sentenced. Do not include any state

reimbursement received by the county for the same purpose.

251