Page 138 - City of Fort Worth Budget Book

P. 138

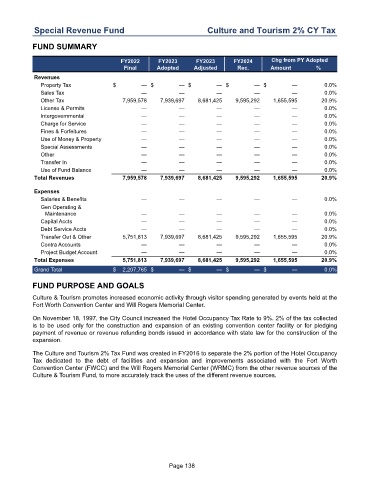

Special Revenue Fund Culture and Tourism 2% CY Tax

FUND SUMMARY

FY2022 FY2023 FY2023 FY2024 Chg from PY Adopted

Final Adopted Adjusted Rec. Amount %

Revenues

Property Tax $ — $ — $ — $ — $ — 0.0 %

Sales Tax — — — — — 0.0 %

Other Tax 7,959,578 7,939,697 8,681,425 9,595,292 1,655,595 20.9 %

License & Permits — — — — — 0.0 %

Intergovernmental — — — — — 0.0 %

Charge for Service — — — — — 0.0 %

Fines & Forfeitures — — — — — 0.0 %

Use of Money & Property — — — — — 0.0 %

Special Assessments — — — — — 0.0 %

Other — — — — — 0.0 %

Transfer In — — — — — 0.0 %

Use of Fund Balance — — — — — 0.0 %

Total Revenues 7,959,578 7,939,697 8,681,425 9,595,292 1,655,595 20.9 %

Expenses

Salaries & Benefits — — — — — 0.0 %

Gen Operating &

Maintenance — — — — — 0.0 %

Capital Accts — — — — — 0.0 %

Debt Service Accts — — — — — 0.0 %

Transfer Out & Other 5,751,813 7,939,697 8,681,425 9,595,292 1,655,595 20.9 %

Contra Accounts — — — — — 0.0 %

Project Budget Account — — — — — 0.0 %

Total Expenses 5,751,813 7,939,697 8,681,425 9,595,292 1,655,595 20.9 %

Grand Total $ 2,207,765 $ — $ — $ — $ — 0.0 %

FUND PURPOSE AND GOALS

Culture & Tourism promotes increased economic activity through visitor spending generated by events held at the

Fort Worth Convention Center and Will Rogers Memorial Center.

On November 18, 1997, the City Council increased the Hotel Occupancy Tax Rate to 9%. 2% of the tax collected

is to be used only for the construction and expansion of an existing convention center facility or for pledging

payment of revenue or revenue refunding bonds issued in accordance with state law for the construction of the

expansion.

The Culture and Tourism 2% Tax Fund was created in FY2016 to separate the 2% portion of the Hotel Occupancy

Tax dedicated to the debt of facilities and expansion and improvements associated with the Fort Worth

Convention Center (FWCC) and the Will Rogers Memorial Center (WRMC) from the other revenue sources of the

Culture & Tourism Fund, to more accurately track the uses of the different revenue sources.

Page 138