Page 9 - Colleyville FY21 Budget

P. 9

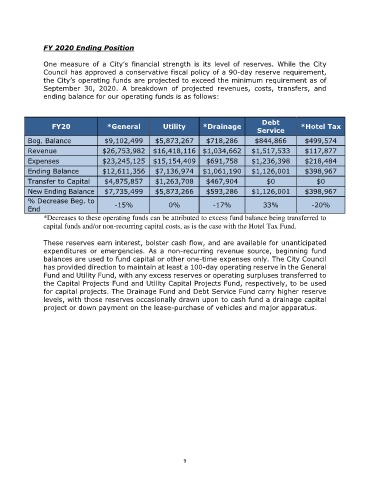

FY 2020 Ending Position

One measure of a City’s financial strength is its level of reserves. While the City

Council has approved a conservative fiscal policy of a 90-day reserve requirement,

the City’s operating funds are projected to exceed the minimum requirement as of

September 30, 2020. A breakdown of projected revenues, costs, transfers, and

ending balance for our operating funds is as follows:

Debt

FY20 *General Utility *Drainage *Hotel Tax

Service

Beg. Balance $9,102,499 $5,873,267 $718,286 $844,866 $499,574

Revenue $26,753,982 $16,418,116 $1,034,662 $1,517,533 $117,877

Expenses $23,245,125 $15,154,409 $691,758 $1,236,398 $218,484

Ending Balance $12,611,356 $7,136,974 $1,061,190 $1,126,001 $398,967

Transfer to Capital $4,875,857 $1,263,708 $467,904 $0 $0

New Ending Balance $7,735,499 $5,873,266 $593,286 $1,126,001 $398,967

% Decrease Beg. to -15% 0% -17% 33% -20%

End

*Decreases to these operating funds can be attributed to excess fund balance being transferred to

capital funds and/or non-recurring capital costs, as is the case with the Hotel Tax Fund.

These reserves earn interest, bolster cash flow, and are available for unanticipated

expenditures or emergencies. As a non-recurring revenue source, beginning fund

balances are used to fund capital or other one-time expenses only. The City Council

has provided direction to maintain at least a 100-day operating reserve in the General

Fund and Utility Fund, with any excess reserves or operating surpluses transferred to

the Capital Projects Fund and Utility Capital Projects Fund, respectively, to be used

for capital projects. The Drainage Fund and Debt Service Fund carry higher reserve

levels, with those reserves occasionally drawn upon to cash fund a drainage capital

project or down payment on the lease-purchase of vehicles and major apparatus.

9