Page 351 - Southlake FY20 Budget

P. 351

CIP

Enhancement Development Corporation, and the Southlake Parks Development Corporation Fund. For FY 2020, the

Capital Budget will be 100% cash funded, eliminating the need to issue bonds.

Bonds

When the City sells bonds, purchasers are, in effect, lending the City money. The money is repaid, with interest, from

taxes or fees over the years. The logic behind issuing bonds for capital projects is that the citizens who benefit from the

capital improvements over a period of time should help the City pay for them. The City can issue bonds in these forms:

• General Obligation (G.O.) Bonds

Perhaps the most flexible of all capital funding sources, G.O. bonds can be used for the design or construction of

any capital project. These bonds are financed through property taxes. In financing through this method, the taxing

power of the City is pledged to pay interest and principal to retire the debt. Voter approval is required if the City

wants to increase the taxes that it levies and the amount is included in the City’s state-imposed debt limits. To

minimize the need for property tax increases, the City makes every effort to coordinate new bond issues with the

retirement of previous bonds.

• Certificates of Obligation (C.O.) Bonds

Similar to general obligation bonds except the certificates require no voter approval. Combination tax and revenue

certificates of obligation are issued for both governmental and business type activities. General obligation bonds,

governmental revenue bonds, and tax notes pledge the full faith and credit of the City. Combination tax and

revenue certificates of obligation are payable from the net revenues of the water and sewer system and general

debt service tax.

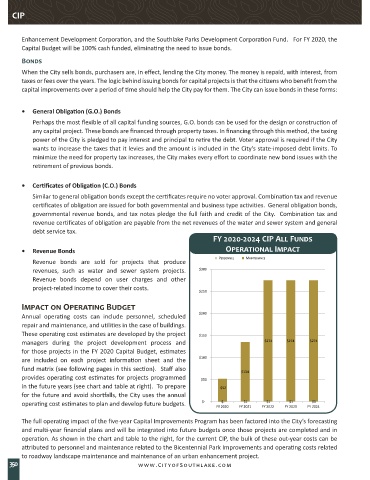

FY 2020-2024 CIP All Funds

• Revenue Bonds Operational Impact

Revenue bonds are sold for projects that produce PERSONNEL MAINTENANCE

revenues, such as water and sewer system projects. $300

Revenue bonds depend on user charges and other

project-related income to cover their costs.

$250

Impact on Operating Budget

Annual operating costs can include personnel, scheduled $200

repair and maintenance, and utilities in the case of buildings.

These operating cost estimates are developed by the project $150

managers during the project development process and $274 $274 $274

for those projects in the FY 2020 Capital Budget, estimates

are included on each project information sheet and the $100

fund matrix (see following pages in this section). Staff also $134

provides operating cost estimates for projects programmed $50

in the future years (see chart and table at right). To prepare $52

for the future and avoid shortfalls, the City uses the annual

$1

operating cost estimates to plan and develop future budgets. $- FY 2020 FY 2021 FY 2022 FY 2023 FY 2024

$1

$1

$-

$1

The full operating impact of the five-year Capital Improvements Program has been factored into the City’s forecasting

and multi-year financial plans and will be integrated into future budgets once those projects are completed and in

operation. As shown in the chart and table to the right, for the current CIP, the bulk of these out-year costs can be

attributed to personnel and maintenance related to the Bicentennial Park Improvements and operating costs related

to roadway landscape maintenance and maintenance of an urban enhancement project.

350 www.CityofSouthlake.com